What Happened the Last Time Markets Were at These Valuations

Last article I showed you where we are: valuations at 1999 levels. Now let me show you what happened next.

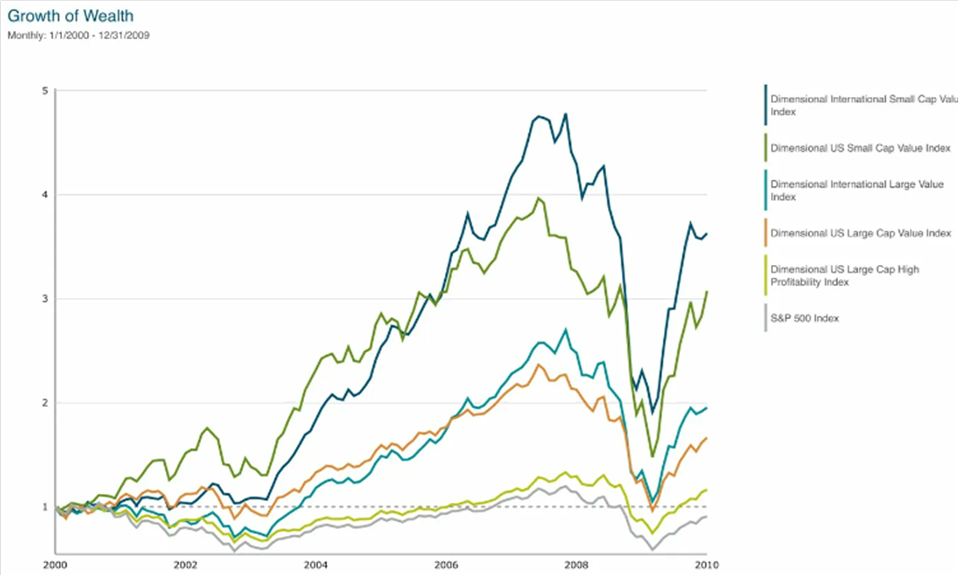

The Lost Decade

If you put £100,000 into the S&P 500 at the start of 2000, ten years later you had £91,000. A whole decade. Negative returns.

Now look at the alternative. That same £100,000 in value strategies:

Dimensional US Small Cap Value: £307,000

Dimensional International Small Cap Value: £363,000

Dimensional US Large Cap Value: £167,000

Same ten years. Same markets. Completely different outcomes.

Why This Happened

When stocks start expensive, they can spend years getting back to normal prices. The companies might do fine. Earnings might grow. But if the stock was overpriced to begin with, the share price goes nowhere.

You're waiting for reality to catch up to expectations. Meanwhile, reasonably priced stocks don't have that problem. When good things happen, the stock price can actually move. There's room for upside.

Japan: An Even Longer Example

The 2000s weren't unique. Japan in 1990 had bubble valuations. Everyone said "this time is different."

Result? Japanese index funds went sideways for 25 years. A quarter century of essentially zero returns.

Value strategies in Japan over the same period? Up 2 to 3 times. This isn't a one-off. It's a pattern.

The Index Fund Strategy

Buying index funds isn't neutral. It's a strategy. And the strategy is: buy the biggest companies. Index funds weight by market capitalisation. Translation: when the biggest companies are expensive (1999, today), you're buying expensive stocks and hoping they get more expensive.

From 2010 to 2021, that worked. Expensive got more expensive.

From 2000 to 2009, it failed. Expensive mean-reverted.

Where We Are Now

We're back at 1999 valuations. Does history repeat exactly? No.

But when you buy stocks at historically high prices, you're betting businesses grow fast enough to justify those prices, or that someone else will pay even more later.

That might happen. But it's worth knowing that's the bet.

What Worked Last Time

Strategies that survived 2000-2009 bought reasonable prices. Two advantages: less downside when expensive stocks corrected, more upside when cheap stocks performed.

Next article: what this means for your portfolio today, and what defensive positioning actually looks like.

For now, the key point: last time we were here, index funds lost a decade while some value strategies tripled.

That's not a prediction. It's a fact worth knowing."